Like half of the millennials in the United States, I opened up a Robinhood account during the peak pandemic trying to move my money out of Betterment and get more actively involved in the day trading scene. Obviously, it ended well for everybody involved.

At some point, like any decent company with a competent strategy team, Robinhood decided to introduce checking accounts for their customers. It was after all, the natural extension of their platform. Now, let's play through this scenario, I want to get money in my Robinhood account from another account. Guess how long this transfer will take? Give or take, five days.

Why? If you are in Fintech or finance, you probably at least have a good idea as to why it takes so long. The reason why access to Robinhood deposits is not almost always immediate is partly due to the nature of ACH payments (which are not processed in real time), but mostly because of the potential risks associated with the transaction. These risks may include insufficient funds, money laundering, fraudulent identity, or other illegal activities. To protect against such risks, it is necessary to carefully review and verify each transaction, which takes time. As a result, access to funds is not instant.

Okay, if you are in Fintech or a bank, you already knew that or at least would have guessed what's the reasons. But let's dive into why it takes so long.

ACH: A Primer

What do Different ACH Payment Types Mean?

So how do I send money to my Robinhood account? It's usually done through an ACH payment. ACH (Automated Clearing House) is a network that was created in the 1970s by banks who wanted to cut down on the use of paper checks, which were the most common way to pay without cash back then. As government organizations like the Social Security Administration started using Direct Deposit payments via ACH instead of paper checks, the ACH network started to become more mainstream.

- At a basic level, the ACH network allows electronic payments between accounts at U.S. banks and other financial institutions. It's made up of rules (set by NACHA) that say how transactions should be coded by a depository institution, who's responsible for fraud, when transactions can be finished, and so on. Two ACH operators – the Federal Reserve and the Electronic Payments Network – make sure that transactions between institutions are settled through the ACH network.

- What is NACHA? NACHA is the National Automated Clearing House Association, a U.S.-based organization that sets rules and standards for the ACH Network. It is a not-for-profit organization that is governed by a board of directors composed of representatives from the financial industry.

- There are two types of ACH transactions - credit and debit transactions. An ACH credit ("push") transaction is a type of electronic payment where the sender initiates the transfer of funds from their bank account to the recipient's bank account. In an ACH credit transaction, the sender "pushes" the funds to the recipient, as opposed to the recipient "pulling" the funds from the sender's account. Typically, ACH credit transactions are initiated using online banking tools. The sender provides the necessary information, such as the recipient's bank account number and routing number, and the funds are transferred electronically. In contrast, an ACH debit ("pull") transaction is initiated by the recipient, who provides the necessary information to their bank and "pulls" the funds from the sender's account. ACH Debit transactions are commonly used for things like online purchases, where the recipient is requesting payment from the sender (think of your phone bills). When you transfer funds from your bank account to Robinhood, the transaction typically uses ACH to debit your bank account. This means that Robinhood initiates the transfer by requesting the funds from your bank account.

- The ACH network is the largest part of the U.S. payments system, accounting for the majority of non-cash payments in the country. In 2018, ACH was used for $64 trillion, or 66% of all non-cash payments, according to the Federal Reserve. In addition to transfers to brokerage accounts like Robinhood, the ACH network also handles a wide range of other transactions, such as electronic bill payments, payroll direct deposits, tax refunds, social security deposits, and many business-to-business payments.

The Automated Clearing House (ACH) system was developed in the 1970s to streamline the process of sending and receiving electronic payments, such as direct deposit of paychecks and electronic bills. The ACH system is operated by the National Automated Clearing House Association (NACHA) and is used by most banks and financial institutions starting from your neighborhood co-op all the way through Marcus by GS. Why is it so popular? ACH allows for the quick and efficient transfer of funds between institutions (and it does so by reducing the need for paper checks and other manual processes). Over the course of the last few decades, the ACH system has evolved to include a wider range of financial transactions, such as e-commerce payments and mobile payments. In 2021 alone, there were 29.11B ACH transactions where $72.62T (yes, it's a big T) was moved using ACH.

- Know Your Customer (KYC)/Anti-Money Laundering (AML) verification: KYC/AML verification is a process that Robinhood and other regulated companies use to verify the identity of their clients and assess their potential risks for money laundering or financing terrorism. In the context of ACH (Automated Clearing House) transactions, KYC/AML verification involves checking the identity of the person or organization initiating the transaction and making sure they are not on any government watchlists or otherwise associated with illegal financial activity. This is important because ACH is a widely used electronic network for financial transactions, and as such, it is a potential target for money launderers and other criminal organizations. By conducting KYC/AML verification, financial institutions can help prevent their systems from being used for illegal purposes.

- If you are a business, there may be additional Know Your Business (KYB) checks as well.

- Here is a short list of companies working on making KYC/AML easier:

- Typically, it is almost instant but can take a few days depending on whether the provider has flagged you or not. If you have been flagged, you may be able to resolve the 'pending' KYC check by providing more documents around your identity. It takes more time for the first transaction than the subsequent ones.

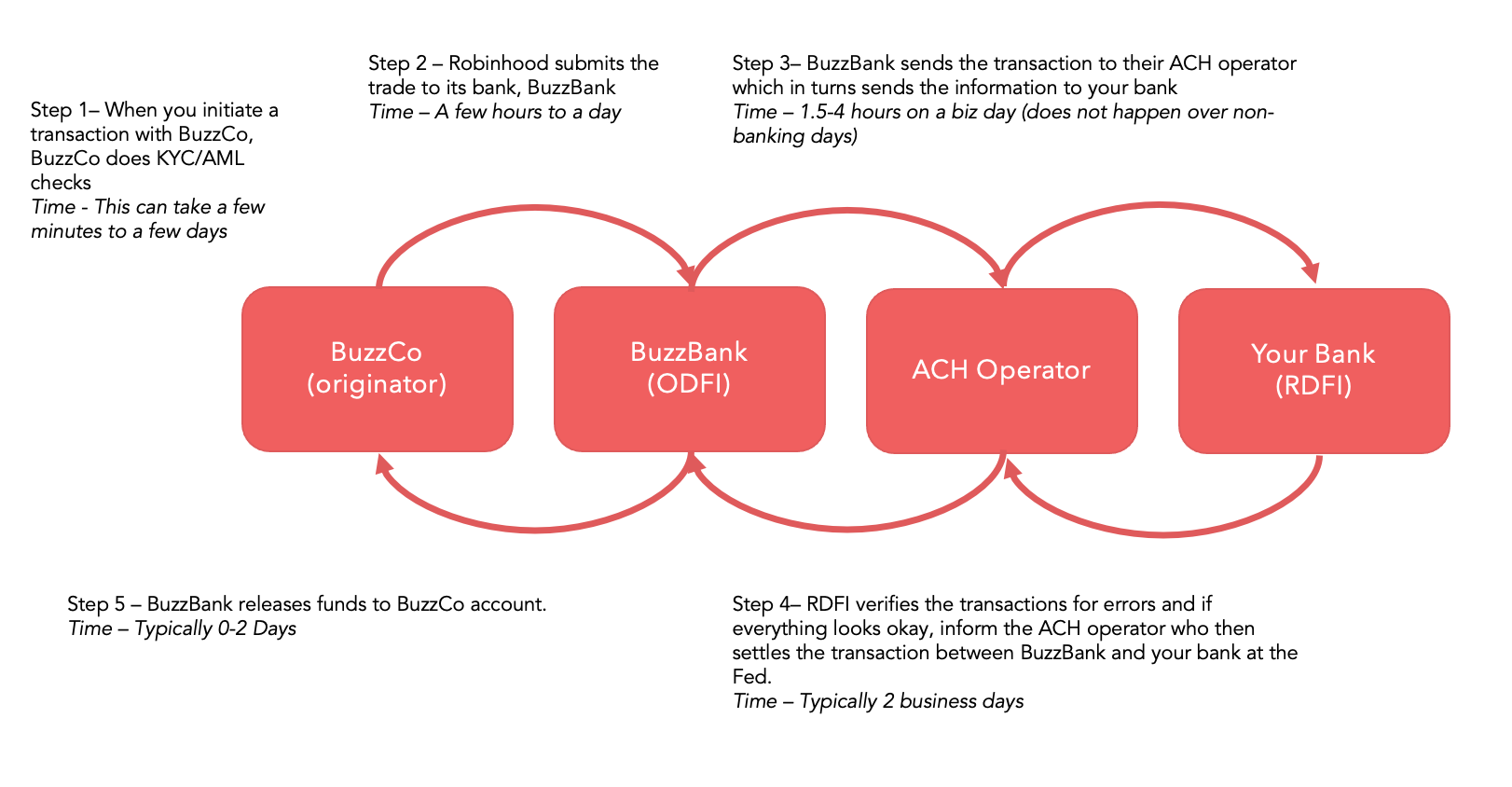

- BuzzCo initiates the transaction by informing BuzzBank, a separate legal entity that custodies funds once they are transferred, of its intention to initiate the transaction. In the past, this would have happened once a day, with BuzzCo sending BuzzBank an ACH file containing all its ACH transactions for the day. Currently, BuzzCo may submit multiple batches of ACH transactions throughout the day and may use a more automated method, such as a money movement API like Modern Treasury or Stripe Treasury to automate all of this.

- Time Taken - Few hours to up to a day depending on how frequently the ACH submission schedule.

- The ACH process involves two operators, The Electronic Payments Network and the Fed, which facilitate the settlement of ACH transactions between banks. When BuzzBank (the originating depository financial institution, or ODFI, because it is initiating the transaction) submits a batch of ACH transactions to one of the operators, the operator separates out the debit transactions and sends them to the banks from which BuzzBank is requesting funds, known as the receiving depository financial institutions (RDFIs) because they are receiving the ACH requests. In the example of BuzzCo, the RDFI is the bank that is funding the BuzzCo account. More on EPN and Fed below.

- The process of verifying and settling ACH transactions at the Receiving Depository Financial Institution (RDFI) involves several steps. After the ACH operator submits the transactions to the RDFI, the RDFI has two business days to review the transactions for errors. These errors can be related to various issues, but one of the most common is insufficient funds in the customer's account. If the customer's account balance is not sufficient to cover the requested debit, the RDFI will generally reject the transaction. In some cases, the RDFI may allow the customer to top up their account balance before settling the transaction, which can cause a delay in the settlement process. If there are no errors, the RDFI will instruct the operator to proceed with settlement. The settlement of ACH transactions between the Originating Depository Financial Institution (ODFI) and RDFI is typically handled through the National Settlement Service, using the Fed Master Accounts of both institutions.

- Time Taken - Typicall 0-2 days

- To complete the process, BuzzBank must release the funds from the ACH transfer into your BuzzCo trading account. However, BuzzBank may wait a couple of extra days to verify that the transaction is legitimate and not fraudulent. This is a necessary precaution for BuzzBank, as it could potentially be responsible for reimbursing any funds that were transferred fraudulently for up to 60 days.

- Time Taken - 0-2 days, depending on risk tolerance

Due to the process above, it is not entirely unimaginable that the transfer can take up to five days.

Innovation and Opportunities

Due to the sheer market size, the opportunity to improve any part of the payment experience is significant

From what we have seen so far, it is clear that when you transfer money from your bank account to a brokerage account, the system and processes are complex due to the risks associated with the transaction and the rules of the ACH system (a remnant of the institutional norms). This complexity can lead to delays, as seen in the example earlier. Unfortunately, these safeguards are necessary to ensure the safety of the payment, but they also mean that some consumers experience slower ACH transfer times as a hedge against the risk.

There have been a number of innovations in risk management within the ACH system in recent years:

- Fraud detection and prevention: Many ACH systems now use advanced algorithms and machine learning techniques to identify and prevent fraudulent transactions. For example, some systems can analyze a user's previous transaction history to detect unusual activity and flag it for further review.

- Risk assessment tools: Some ACH systems now offer risk assessment tools that allow financial institutions to evaluate the risk level of a particular transaction or account. These tools can help banks and other financial institutions make more informed decisions about whether to approve or reject a transaction.

- Enhanced security measures: ACH systems have also implemented additional security measures to protect against fraud, such as two-factor authentication and secure socket layer (SSL) encryption.

- Risk management policies and procedures: ACH systems have also developed and implemented more robust risk management policies and procedures to help prevent and mitigate risk. These may include measures such as regular risk assessments, employee training, and the development of risk management plans.

- Collaboration and information sharing: ACH systems have also worked to improve collaboration and information sharing among financial institutions in order to better identify and prevent risk. This may include sharing best practices, collaborating on risk assessment tools and techniques, and establishing forums for information sharing.

The end theme for some of these big areas are to either bring down the fraud rates, reduce the time to transaction completition, or to improve trust within the system.

RTP - The Next Chapter In Real Time Payments?

Real-time payments (RTP) are electronic payment systems that allow for the immediate transfer of funds from one bank account to another, usually within seconds or a few minutes. RTP systems differ from traditional payment methods, such as checks or Automated Clearing House (ACH) transactions, which can take several days to process.

RTP systems are designed to be efficient, convenient, and secure, allowing individuals and businesses to make and receive payments quickly and easily. They are often used for urgent or time-sensitive payments, such as paying bills or sending money to friends and family. RTP systems are supported by banks and financial institutions, and are available through various channels, including online banking, mobile apps, and ATMs.

There are several different RTP systems in use around the world, including the U.S. Federal Reserve's Same Day ACH, the European Central Bank's TIPS, and the UK's Faster Payments Service.

I will be writing more about RTP at some point, but it is worth pointing out that there are so many other competing systems being developed for real time settlements.